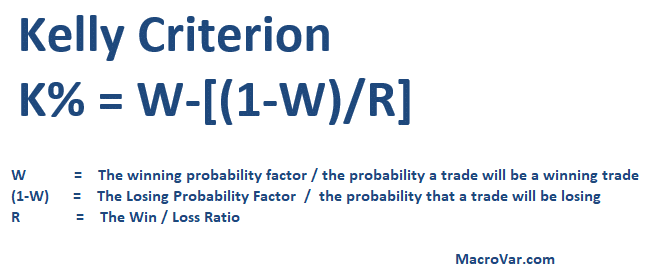

Analysing & formula of the Kelly criterion

The Kelly criterion is a formula used in investing to calculate the optimal amount that should be allocated in future trades based on historical performance.

Suppose you run a trading portfolio and you know your past trading historical performance. The Kelly Criterion tells you the position sizes you should be taking on your next trade.

Kelly criterion formula

Kelly Criterion Example

The steps to use Kelly Criterion are the following:

Step 1: Calculate W. W is the winning probability factor. If for example your portfolio has 20 winning trades out of 40 total trades your W is 20 / 40 = 0.50. This means the trades has made money on half of his trades.

Step 2: Calculate R. R is the win/loss ratio. If for example your portfolio’s winning trades earned $250,000 while your losing trades lost $130,000 your R is 250,000/130,000 = 1.92. This means that the trader, has made 1.92 times what he loses on losing trades.

Step 3: Calculate Kelly %. Given the formula provided above the Kelly % is calculated as follows: 0.50-[(1-0.50/1.92] = 23.96%

Based on the Kelly Criterion and you past performance you should allocate 23.96% of your capital on the next trade, in order to maximise portfolio’s performance.

Conclusions

If R remains constant K increases as the trader’s W increases. That is Kelly criterion suggests to take larger risk in the next trade if a trader is right more of the time and vice-versa.

If W remains constant K increases as the trade’s Win/Loss ratio (R) improves. That is Kelly criterion suggests to take larger risk in the next trades if a trader makes more money from each trade.

Kelly Criterion Calculator

Sign up free to download MacroVar Kelly Criterion calculator in Excel.

[content_control]

[/content_control]

Optimal Capital allocation and leverage

Suppose an investor has to trade several strategies, each with specific expected returns and standard deviations based on the historical performance. Kelly criterion will help him find the optimal way to allocate capital among them. Furthermore, Kelly criterion will also estimate the overall leverage (ratio of size of portfolio to account equity).

The aim of Kelly criterion is to maximise the investor’s long-term wealth. Maximising long-term wealth is equivalent to maximizing the long-term compounded growth rate g of the portfolio. To simplify matters Kelly criterion will assume a gaussian probability distribution for each trading strategy i with a fixed mean m, and standard deviation si. The returns are net of all financing costs. The optimal allocation of equity for each of n strategies is a column vector F* = (f1*, f2*,… fn*). If we assume strategies are statically independent, the kelly criterion formula is:

where fi is % of capital allocated to each strategy, mi is each strategy’s mean returns and si is each strategies standard deviation.

Because of uncertainties in parameter estimations, and the fact that the distribution of returns is not Gaussian, traders prefer to cut the recommended leverage in half. This is called half-kelly betting.

The maximum compounded growth rate is: g = r + S^2

where S is the Sharpe ratio of the portfolio.