The Universal Investment Strategy rebalance every month on some multiple of 5% between SPY and TLT that previously maximized the following quantity (returns/vol^2.5 on a 72-day window).

MacroVar offers 300+ Investment Strategies with higher returns, lower risk and losses than the TU Momentum Strategy

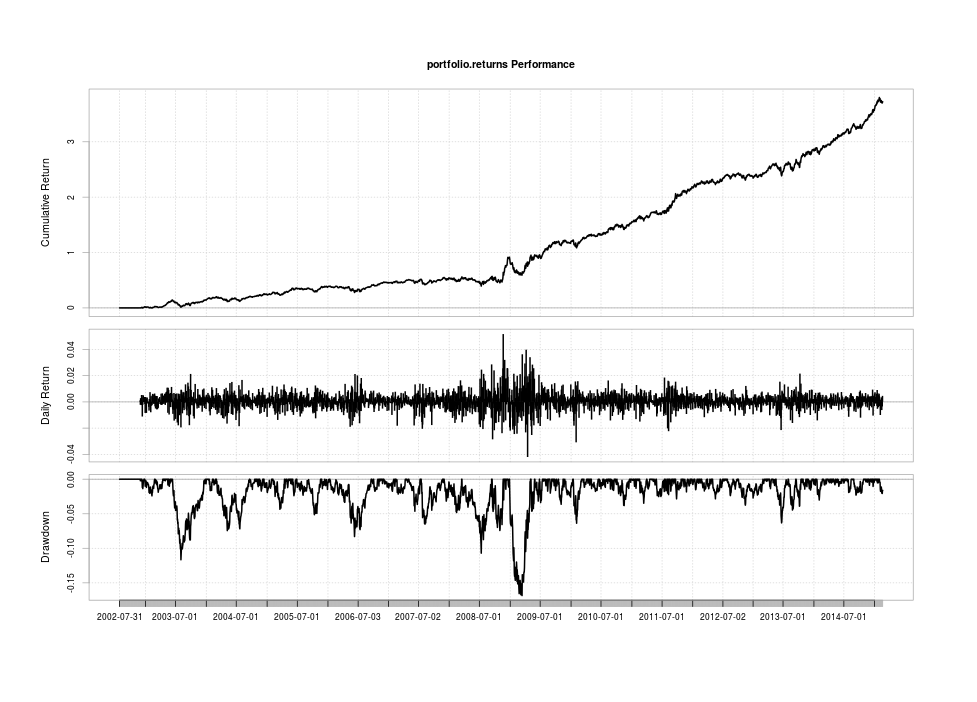

Investment Performance

Investment Return (?):

13.17%

Volatility (?):

9.90%

Sharpe Ratio:

1.33

Maximum Drawdown:

-16.80%

Investment’s Fundamental Concept:

The concept on which the strategy is based uses a walk-forward methodology of maximizing a modified Sharpe ratio, biased heavily in favor of the volatility rather than the returns. That is, it uses a 72-day moving window to maximize total returns between different weighting configurations of a SPY-TLT mix over the standard deviation raised to the power of 5/2. To put it into perspective, at a power of 1, this is the basic Sharpe ratio, and at a power of 0, just a momentum maximization algorithm.

Investment’s Logic:

The process for this strategy is the following: rebalance every month on some multiple of 5% between SPY and TLT that previously maximized the following quantity (returns/vol^2.5 on a 72-day window).

The concept on which the strategy is based uses a walk-forward methodology of maximizing a modified Sharpe ratio, biased heavily in favor of the volatility rather than the returns. That is, it uses a 72-day moving window to maximize total returns between different weighting configurations of a SPY-TLT mix over the standard deviation raised to the power of 5/2. To put it into perspective, at a power of 1, this is the basic Sharpe ratio, and at a power of 0, just a momentum maximization algorithm.

Other Investment Strategy Characteristics:

Investment Type:

Momentum Strategy

Investment Risk:

2/5 Low

Backtest Range:

30-40 years

Rebalancing period:

Daily

Investment Strategy Markets:

Dow Jones Stoxx 50 index futures (FSTX)

Get Unlimited access to our database for Free by inviting your friends to MacroVar

Help your friends make the right business & financial decisions using free MacroVar analytics. Click here to invite them and get upgraded for free.